Thinking outside the box: Seneca Global Income and Growth Trust

Disclosure – Non-Independent Marketing Communication. This is a non-independent marketing communication commissioned by Seneca Global Income & Growth Trust. The report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on the dealing ahead of the dissemination of investment research.

![]()

Kepler Trust Intelligence looks at the unique approach to value investing taken by Seneca Global Income & Growth Trust…

Following the stock market crash that we saw in March of 2020, and subsequent falls after concerns over a second wave of COVID-19, a wide range of UK shares – already some of the most unloved equities in the world in part thanks to the rancour surrounding Brexit negotiations and the uncertainty of the future trading conditions for UK companies– are now trading at what seem like extraordinarily low valuations.

Clearly this is perhaps justified in many cases, as companies have been dramatically impacted by COVID-19 and therefore are suffering with weaker, and often precarious, financial positions and outlooks.

However, such is the aversion to risk which we are seeing, that, amongst any company which is not more or less explicitly tied to internet retail or technology, there seems very little distinction made between these vulnerable companies and others which are in far better shape.

This makes for a rich hunting ground for contrarian investors, seeking returns from companies which are outside of the ‘usual suspects’ group of high growth stocks.

Seneca Global Income & Growth Trust (SIGT) – as a globally diversified multi-asset trust – may not be an obvious choice for UK exposure. However, with 30% of the portfolio in UK equities, it offers flexible and differentiated exposure to any UK recovery.

While a recovery may yet be some time away, investors in SIGT are currently being ‘paid to wait’ with an attractive current yield of 4.6% which the board opted to maintain this year part-funded by reserves and will review again in 2021 given the challenging economic conditions.

Value, but not as you know it…

There is no way of knowing how much time it will take for sentiment to recover after the market crash. However, history shows that over the long term this should ultimately correct itself.

Typically markets overreact to the potential for calamity; once the air clears and fears recede, stocks are typically left in a position to deliver above-average returns.

Furthermore, the UK economic outlook could improve going forward, with stock market valuations essentially suggesting there is no realistic prospect of economic recovery. Alongside this, should a Brexit deal be achieved further impetus would be given to a market which abhors uncertainty.

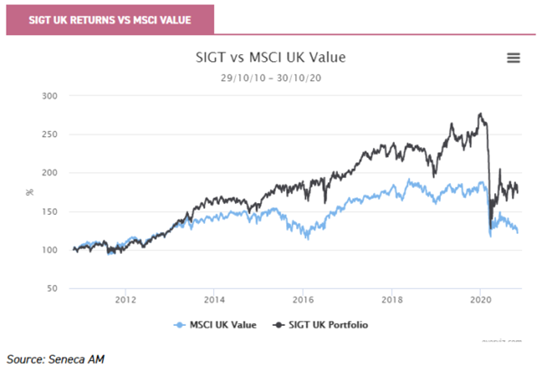

SIGT are looking to take advantage of this and have a clearly demonstrated track record of success in doing so. Over the past decade we have seen ‘value’ companies drastically underperform growth, as can be seen below.

However, with good selection there have seen been some excellent returns even in this unloved sector. This is shown below, with the trust dramatically outperforming the wider value index.

Although valuation underpins the stock-selection process, stock positions are not initiated solely on the expectation of valuation uplift to drive returns. Instead, the team are look for opportunities in stocks with strong operational positions.

A recent example of a company like this is Purplebricks. The team have long had the company on their watchlist, however the elevated valuation level and concerns over the non-core (and non-profitable) US and Australian businesses meant they had previously held off.

However, the market correction saw a sharp de-rating and the management of Purplebricks also decided to exit the previously mentioned non-core businesses. As such, the team at SIGT used this opportunity to invest in the company, believing that the stock was subsequently undervalued and misunderstood.

Previously, the stock was rated at similar levels to that of a pure technology company, and any revaluation to a similar level would offer very sizeable upside, in addition to the potential for operational growth which the business possesses.

Similarly, the team are able at present to identify companies which show structural growth opportunities likely to feed into enhanced dividends, but where the perceived exposure to cyclical economic pressures continues to weigh on the share price valuation.

This can be seen in their holding in Vistry, the UK housebuilder. Perceived as a ‘cyclical’ stock because of the nature of its business, Vistry presently trades at below its reported book value, and below reported revenues.

Whilst its business has been impacted by the COVID-19 pandemic and associated economic shutdown, there remains an imperative to build more housing stock in the UK, with mooted reforms to planning laws perhaps catalysing this.

Accordingly, the sector as a whole should enjoy tailwinds to top-line growth, which Vistry, as one of four main players, stands to benefit from.

Even on conservative assumptions regarding housing prices, including sharp falls, Vistry should remain profitable on individual housing units and projects, and currently exhibits strong profit margins on existing projects.

This might allow them to resume their dividends next year after a precautionary halt earlier in 2020, and investors could possibly see a progressive dividend policy come into place in the future.

While waiting for these opportunities to potentially grow and re-rate, investors can enjoy a dividend from the trust as mentioned above. SIGT has a long term total return mandate, to which dividends will contribute.

The majority of the income generation comes from equities and alternatives and is diversified by both asset classes and geography as we discuss in our recent research note here.

The global market and macroeconomic outlooks remain fraught with uncertainty, and the UK market has struggled. Historically the UK market is associated as open and, by extension, more vulnerable than many peers to fluctuations in the global cycle.

However, market level valuations in the UK are severely discounted relative to other global markets, and fund manager surveys continue to indicate the UK remains a significant underweight allocation amongst institutions. This suggests to us that any risks specific to the UK at the market level are already priced in, and likely more.

Furthermore, whilst certain UK companies and sectors look vulnerable, many of these valuation opportunities are in companies likely to prove operationally robust.

There could thus be a double opportunity in the UK market. The UK market itself could well display additional upside to global peers on any evidence of economic recovery and/or normalisation, as the insolvency risks priced into many stocks recede; current discounted market valuations suggest concerns are more elevated around these risks than other markets.

And these risks look mispriced at the company-specific level in many cases, irrespective of whether we see a rapid economic recovery or a more gradual one.

If the global economy starts once again to contract, downside risk looks more accurately priced into these stocks than many others, and global equities will highly likely struggle in any event. SIGT’s significant UK equity exposure aims to access areas where such an asymmetric relationship exists.

With the IMF’s chief economist calling for mass fiscal support of global economies and a likely definitive resolution to Brexit negotiations, along with a result in the US election, it seems eminently possible that global sentiment towards the economic outlook could rapidly shift to a more positive footing, despite recent reintroductions of lockdowns.

SIGT’s equity book seems well placed to benefit in such a scenario. Yet this is balanced within a multi-asset exposure, with a significant allocation to alternatives and protective strategies which should offer the portfolio downside protection in a more negative scenario.

To learn more about how SIGT are refining value investing, read the full report here…

![]()

To buy this trust login to your EQi account

Select Seneca Global Growth and Income Trust GB0008769993

Disclaimer

This report has been issued by Kepler Partners LLP. The analyst who has prepared this report is aware that Kepler Partners LLP has a relationship with the company covered in this report and/or a conflict of interest which may impair the objectivity of the research.

Past performance is not a reliable indicator of future results. The value of investments can fall as well as rise and you may get back less than you invested when you decide to sell your investments. It is strongly recommended that if you are a private investor independent financial advice should be taken before making any investment or financial decision.

Kepler Partners is not authorised to market products or make recommendations to retail clients. This report has been issued by Kepler Partners LLP, is based on factual information only, is solely for information purposes only and any views contained in it must not be construed as investment or tax advice or a recommendation to buy, sell or take any action in relation to any investment.

The information provided on this website is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject Kepler Partners LLP to any registration requirement within such jurisdiction or country. In particular, this website is exclusively for non-US Persons. Persons who access this information are required to inform themselves and to comply with any such restrictions.

The information contained in this website is not intended to constitute, and should not be construed as, investment advice. No representation or warranty, express or implied, is given by any person as to the accuracy or completeness of the information and no responsibility or liability is accepted for the accuracy or sufficiency of any of the information, for any errors, omissions or misstatements, negligent or otherwise. Any views and opinions, whilst given in good faith, are subject to change without notice.

This is not an official confirmation of terms and is not a recommendation, offer or solicitation to buy or sell or take any action in relation to any investment mentioned herein. Any prices or quotations contained herein are indicative only.

Kepler Partners LLP (including its partners, employees and representatives) or a connected person may have positions in or options on the securities detailed in this report, and may buy, sell or offer to purchase or sell such securities from time to time, but will at all times be subject to restrictions imposed by the firm’s internal rules. A copy of the firm’s Conflict of Interest policy is available on request.

Read the latest edition of DIY Investor Magazine

DIY Investor Magazine

The views and opinions expressed by the author, DIY Investor Magazine or associated third parties may not necessarily represent views expressed or reflected by EQi.

The content in DIY Investor Magazine is non-partisan and we receive no commissions or incentives from anything featured in the magazine.

The value of investments can fall as well as rise and any income from them is not guaranteed and you may get back less than you invested. Past performance is not a guide to future performance.

DIY Investor Magazine delivers education and information, it does not offer advice. Copyright© DIY Investor (2016) Ltd, Registered in England and Wales. No. 9978366 Registered office: Mill Barn, Mill Lane, Chiddingstone, Kent TN8 7AA.