Why are UK mid caps in such an M&A sweetspot right now?

![]()

UK-quoted companies are attracting good interest as global deal-making picks up again and FTSE 250 companies appear to be the candidates of choice

By Jean Roche, Fund Manager, Schroder UK Mid Cap Fund plc

It would be difficult to miss the fact that UK mid cap companies are attracting a renewed level of bid interest at present. So much so that, every morning, when I log in to my virtual workplace, I am mentally preparing myself to see a new headline about the next one to be bid for.

In particular, renewed demand for UK-quoted companies from large and experienced foreign buyers suggests to me that other investors continue to overlook an opportunity. Mid cap companies are at the centre of this interest from overseas companies (so-called “strategic buyers”), private equity (PE) or PE-backed purchasers.

It’s always helpful to observe what the corporate and PE sectors are doing since we share their long-term mentality. If the pick-up in “inbound” activity is a guide, it seems to me these bidders are currently thinking: “UK shares are cheap, sterling is weak, this is our opportunity to buy some prized assets outright.”

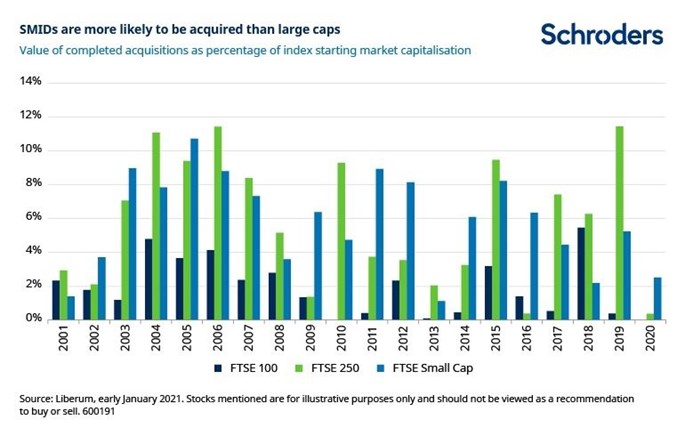

Mid caps are a synonym for the FTSE 250 index, which is the next most established group of shares trading on the London Stock Exchange outside the FTSE 100. These companies can be the target of choice for bidders – not too big, but sufficiently large to make a difference – and in 2019 close to 12% of the FTSE 250 was acquired (see below).

Global deal-making has resumed with gusto as debt financing has cheapened again, with policymakers slashing interest rates and restarting monetary easing in response to Covid-19.

The crisis has also accelerated a number of structural trends and companies are either re-sizing their operations or capitalising on opportunities with the help of M&A.

Against this backdrop, could 2021 be another vintage year for mid cap M&A? At present it seems very possible.

Overseas bidders tussle for control

We’ve seen a tussle for mid cap bookmaker William Hill, where the eponymous owner of Las Vegas’s iconic casino Caesars has seen off PE group Apollo.

Meanwhile, two North American rivals (both of them PE backed) appear at the time of writing to still be vying for FTSE 250 security group G4S.

More recently, US PE groups Blackstone and Carlyle have been in competition for control of Signature Aviation. At the time of writing the mid cap aviation services company had recommended a bid from Global Infrastructure Partners, a US infrastructure fund manager.

To my mind, this interest is further evidence of the opportunity offered by UK shares, which remain in the doldrums.

While UK shares have responded well to the vaccine news in early November, and then again to the Brexit trade deal, there is an awful lot of lost ground to make up after four and half years of Brexit uncertainty.

Bidders appear to be sensing a window of opportunity, with valuations still low but uncertainty removed by the Brexit deal. At the same time, good progress with the UK’s Covid-19 immunisation programme gives a glimpse of sunlight at the end of the tunnel, as opposed to the headlights of a train running at full speed.

Whilst certainty is in short supply in many ways, we do know that the economy will, at some point, be able to properly open up again (see What happens when the party starts back up?).

Portfolio refreshment like no other

If the experience from 2019 is anything to go by, all variety of mid cap companies could be in the frame for a bid.

Those snapped up last time ranged from air-to-air refuelling specialist Cobham (sold to US PE group Advent) to Suffolk brewer Greene King, which was bought by Hong Kong-based investors.

Hasbro of the US purchased mass media group Entertainment One, and Blackstone (alongside the investment company of The Lego Group’s Danish founding family) bought back theme park operator Merlin Entertainments. US PE firm Thoma Bravo acquired cyber security business Sophos.

Aside from shining a light on the unloved status of UK shares, such M&A activity helps make room for the next tranche of exciting mid cap companies in a rapidly-evolving world.

These can be new (or returning companies) which join the stock market via initial public offerings (IPOs). They can also be small cap companies vying for promotion to the FTSE 250 – for this reason we’re also always watching M&A and IPO activity lower down the market for tomorrow’s potential mid caps.

Since mid caps are generally better able to capitalise on new opportunities than their larger counterparts, they tend to be more dynamic – it also helps to have a smaller base from which to achieve growth.

For all of these reasons, we’re often heard referring to the FTSE 250 as the “Heineken Index”, given its potential to “refresh” a portfolio in a way other parts of the market can’t. Cheers!

More information about the Schroder UK Mid Cap Fund plc >

To buy this trust login to your EQi account

Select Schroder UK Mid Cap Fund plc - GB0006108418

Important information

This communication is marketing material. The views and opinions contained herein are those of the named author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations. Information herein is believed to be reliable but Schroder Investment Management Ltd (Schroders) does not warrant its completeness or accuracy.

The data has been sourced by Schroders and should be independently verified before further publication or use. No responsibility can be accepted for error of fact or opinion. This does not exclude or restrict any duty or liability that Schroders has to its customers under the Financial Services and Markets Act 2000 (as amended from time to time) or any other regulatory system. Reliance should not be placed on the views and information in the document when taking individual investment and/or strategic decisions.

Past Performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of any overseas investments to rise or fall.

Any sectors, securities, regions or countries shown above are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

The forecasts included should not be relied upon, are not guaranteed and are provided only as at the date of issue. Our forecasts are based on our own assumptions which may change. Forecasts and assumptions may be affected by external economic or other factors.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England. Authorised and regulated by the Financial Conduct Authority.

Click to visit:

Read the latest edition of DIY Investor Magazine

DIY Investor Magazine

The views and opinions expressed by the author, DIY Investor Magazine or associated third parties may not necessarily represent views expressed or reflected by EQi.

The content in DIY Investor Magazine is non-partisan and we receive no commissions or incentives from anything featured in the magazine.

The value of investments can fall as well as rise and any income from them is not guaranteed and you may get back less than you invested. Past performance is not a guide to future performance.

DIY Investor Magazine delivers education and information, it does not offer advice. Copyright© DIY Investor (2016) Ltd, Registered in England and Wales. No. 9978366 Registered office: Mill Barn, Mill Lane, Chiddingstone, Kent TN8 7AA.